Biden takes a wrong step

I was sorry to see President Biden threaten steel tariffs on antidumping grounds. For my views on this topic, see this old piece I wrote with Phill Swagel, who is now CBO director.

Random Observations for Students of Economics

I was sorry to see President Biden threaten steel tariffs on antidumping grounds. For my views on this topic, see this old piece I wrote with Phill Swagel, who is now CBO director.

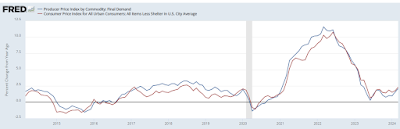

Click on image to enlarge.

This figure shows that the PPI for final demand tracks the CPI less shelter very closely. By both measures, inflation is now very much under control. The problem is that the CPI for shelter is up 5.6 percent, so the overall CPI looks quite hot.

Some would argue that leaving out shelter is misleading because shelter is such a large fraction of the typical household budget. On the other hand, the CPI for shelter is well known to be a lagging indicator of rents by virtue of how it is constructed, and other more current series show no recent inflation in rents. This latter argument puts me in the optimistic camp on inflation.

By the way, I recently made a bet with my friend Larry Ball that the overall CPI from February 2024 to February 2025 will rise by less than 2.5 percent. I am writing the bet here as a sort of contract. We will check back next year.

The bet is for $5. That is in nominal terms. So, in real terms, I get more if I win than Larry gets if he wins.

My friend Yoram Bauman, the stand-up economist (who I first met because of his parody of my ten principles), says he’s working on a play... and that it’s a romantic comedy about carbon tax ballot measures! Details on his Kickstarterpage and his blog.

In watching part of Jay Powell's news conference yesterday, I realized that what he is doing to just the opposite of good economics communication. When I write an article, give a lecture, or draft a textbook chapter, my goal is to convey maximum information in the fewest words possible. But when the Fed chair answers reporters' questions, he seems to be conveying the least possible information in the most words possible.

Every answer the Fed chair gives is, more or less, a new paraphrasing of what the FOMC has already said in their statement or the chair has said many times before. From the Fed's perspective, the ideal news conference contains no news and is mainly repetition and platitudes. "Our decisions are data-dependent....The future is uncertain....Blah blah blah...."

It is almost as if the news conference should come with a disclaimer: "I do not intend to say anything interesting. If you think I have said something interesting, please ignore because I misspoke."

Here is my recommendation: Stop giving news conferences. The Fed's policy decision and statement should stand by themselves. The Supreme Court does not give news conferences after announcing decisions. They explain their judgment once in writing and then let that stand. The Fed should do the same.

Grad students with an interest in the history of economic thought should click here.

Did you know that Kendall Roy (of Succession fame) graduated from the Harvard economics department? You can bid on his diploma here. He must have been in ec 10, though I don't recall him.

Click on image to enlarge.

...based on relevance for central banks. At the top is the Brookings Papers on Economic Activity, followed by the Quarterly Journal of Economics and the Journal of Monetary Economics.

In recent years, I have been teaching a seminar to a small group of Harvard freshmen. I described the seminar in this essay in the NY Times.

The assigned readings change a bit from year to year. In case any of my blog readers are interested, here are the books I chose for this year:

These TV shows aren't new, but they were new to me, and I enjoyed them both: Borgen (a Danish political drama) and Caliphate (a Swedish drama about an impending ISIS attack). Both are on Netflix, available dubbed in English or in the original language with subtitles. Thanks to Olivier Blanchard for the Borgen recommendation.

This graph from David Leonhardt's column is illuminating. Now I understand why those of us who are fiscally conservative and socially liberal have trouble finding political candidates to fully represent our views. There are too few of us!

I am the Robert M. Beren Professor of Economics at Harvard University. I use this blog to keep in touch with my current and former students. Teachers and students at other schools, as well as others interested in economic issues, are welcome to use this resource.